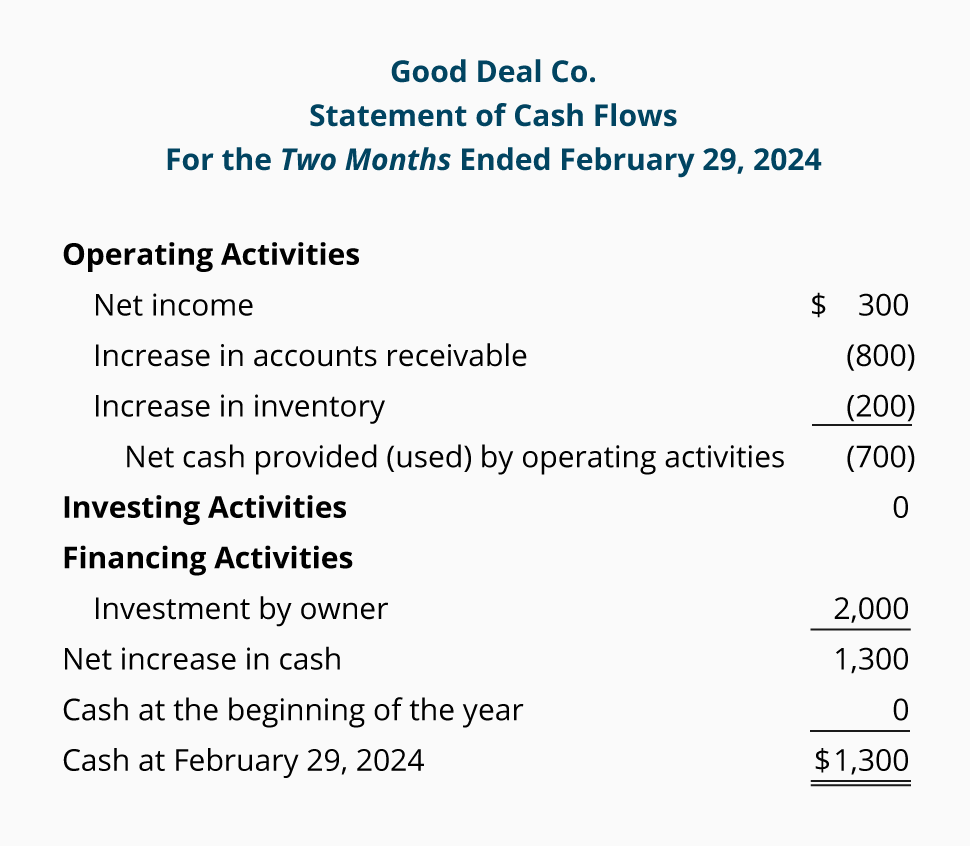

Fine Beautiful Note Payable Cash Flow

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Provision For Bad Debts Create Financial Projections

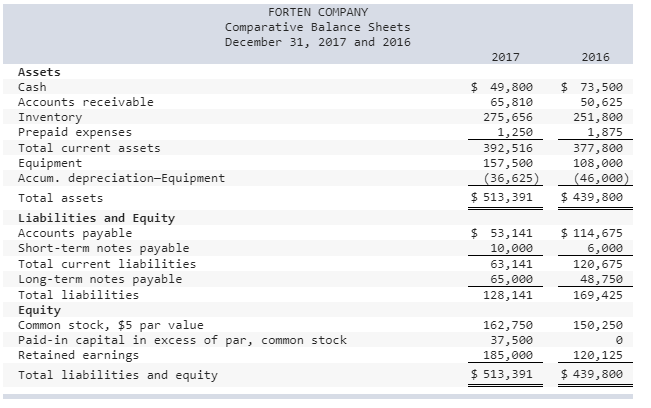

Quiz And Homework Chapter 12 Indirect Statement Of Cash Flows Pg&e Balance Sheet Revenue Accounts Normally Have Debit Balances

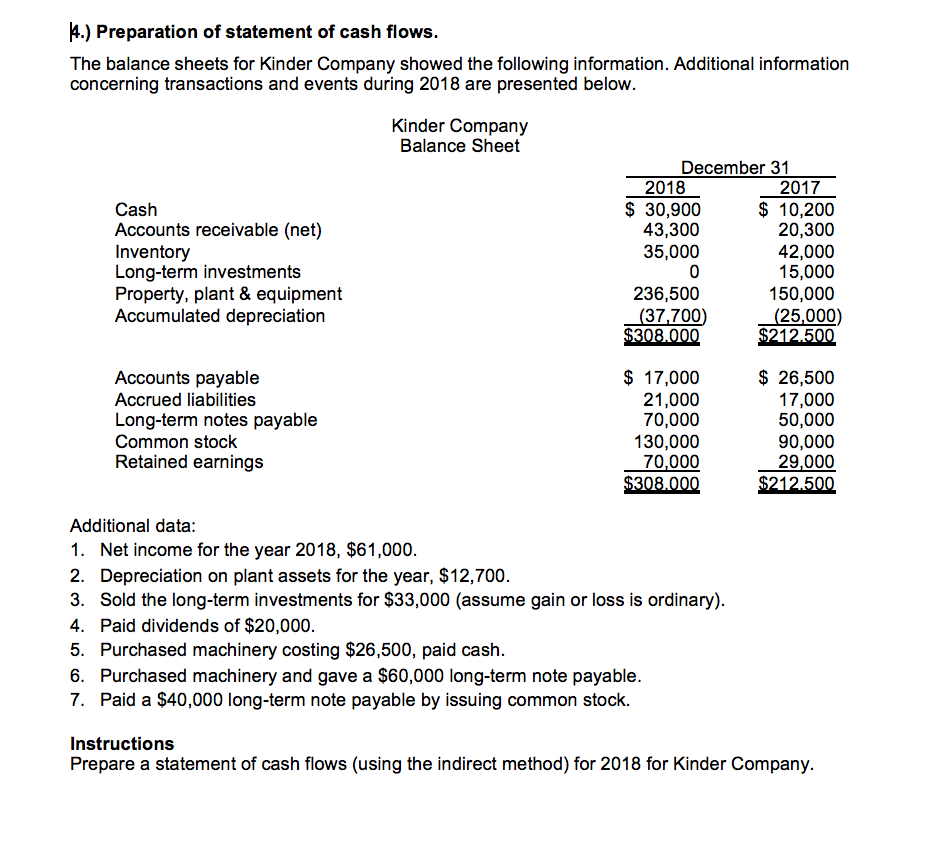

4 Preparation Of Statement Cash Flows The Chegg Com Ben And Jerrys Financial Statements Rms Accounting Firm

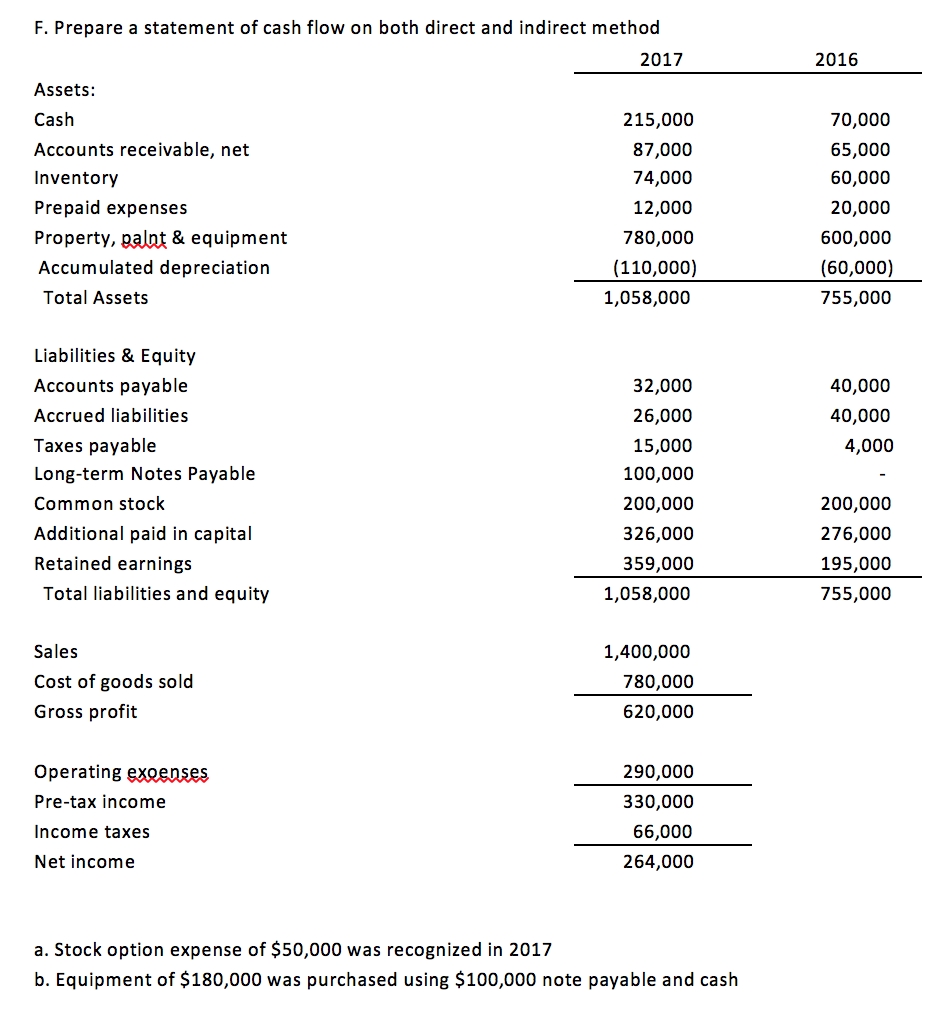

F Prepare A Statement Of Cash Flow On Both Direct Chegg Com Profit And Loss Income Will Be Which Side Free Projection Template

The Statement Of Cash Flows Think To Scale Monthly Profit And Loss Template Excel Uk Difference Between P&l Flow

Read E Book Cash Flow Notes Capital Reserve In Statement Financial Of Mang Inasal

Cash payments to employees for services including benefits Note.

Note payable cash flow. Cash payments to suppliers of goods and services. Cash flow from financing activities are activities that result in changes in the size and composition of the equity capital or borrowings of the entity. A business reports this amount as a cash inflow in the financing activities section of the cash flow statement.

The statement of cash flows explains the changes in the balance sheet during an accounting period from the perspective of how these changes affect cash. Examples of financing cash flows include cash proceeds from issuance of debt instruments such as notes or bonds payable cash proceeds from issuance of capital stock cash payments for dividend distributions principal repayment or redemption. Separate accounts payable and payroll payable when determining the cash payments.

Interest payments on a note payable do not change the notes payable account but. On the other hand interest paid shows up in cash flow to creditors but not repayments of note principal which show up in the change in NWC. A A decrease in cash flows from investing activities.

In both contexts NWC is essentially treated as an asset which means that notes payable have been netted out treated as a contra-asset. A business reduces its notes payable account when it makes a payment toward a notes. Determine Net Cash Flows from Operating Activities.

When a business takes on a new loan or note it increases the notes payable account on the balance sheet. The interest paid on a note payable is reported in the section of the cash flow statement entitled cash flows from operating activities. The interest rate and frequency of payments are parts of the note agreement.

Cash is debited and Notes Payable is credited for 5000. How is the amortization of patents reported in a statement of cash flows that is prepared using the indirect method. Interest Payments on a Note Payable.

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Cecl Credit Loss Calculate From Operating Activities

Is Short Term Notes Payable A Financing Activity Financeviewer Preliminary Financial Statements Statement Analysis Of Non Sector 2018

Reporting The Statement Of Cash Flows Ppt Download A Inflow From Financing Activities Includes Financial Nestle 2018

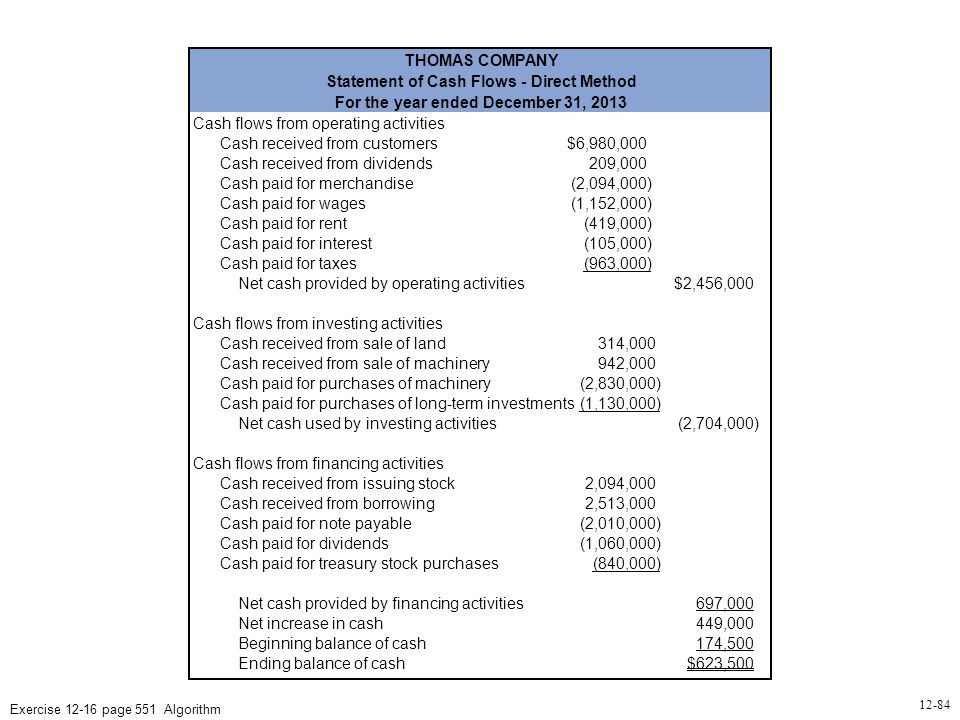

Chapter 12 Reporting And Analyzing Cash Flows Click On Links Exercise 4 Page 547cash Flow From Operations Indirectexercise Algo Ppt Download Purpose Of Vertical Analysis Typical P&l Statement

Cash Flow Statement Example Financial Analysis Wikipedia Free Calculation From

How Do Net Income And Operating Cash Flow Differ Actblue Charities Financial Statements Doubtful Debts In Balance Sheet

Methods For Preparing The Statement Of Cash Flows Flow Direct Method Reading Financial Reports Dummies Md&a Analysis

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is Examples Investment In Subsidiary Ifrs A P&l Account