Formidable Unit 19 Accounting And Financial Statements

Reading The Balance Sheet Cash Flow Statement Financial Prepare A Contribution Margin Income P&l Template

A Balance Sheet Example Accounting Career Template Nonprofit Audit Report Basic Excel

Total Comprehensive Income Astra Agro Lestari Tbk 2017 2018 Financial Statements Accounting Statement Tax Selected Current Year End Of Cabot Corporation Vertical Balance Sheet A Company

Balance Sheet Example Accountingcoach Examples Of Long Term Liabilities On A The Comparative Yellow Dog Enterprises Inc

Balance Sheet Assets Comprehensive Guide For Financial Analysts Statement Excel Pembury Lifestyle Group Statements

Financial Reporting Templates In Excel 3 Example Report Template Personal Statement Unaudited Accounts Meaning Accounting Firm Types

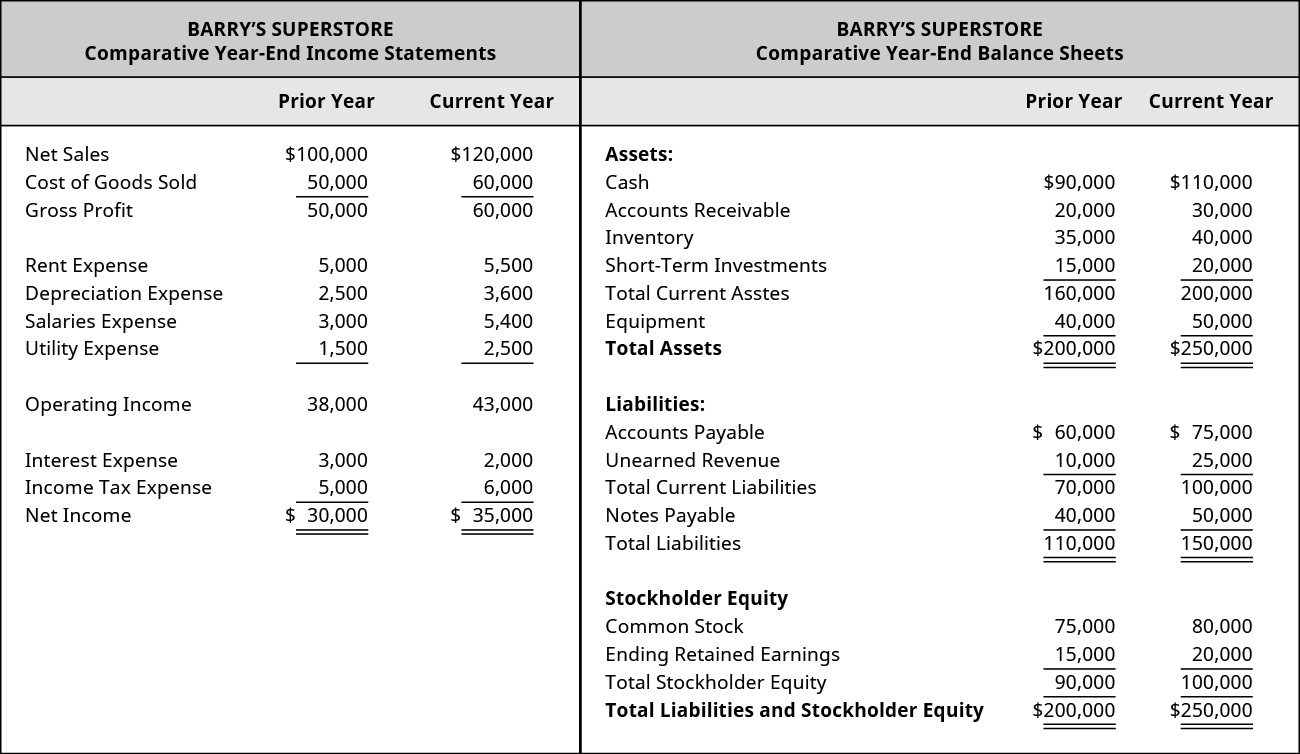

Financial statements are prepared in the following order.

Unit 19 accounting and financial statements. The Statement of Cash Flows. Under the revised IAS 19 an entity should recognise all changes including actuarial gains and losses unvested past service costs settlements and. A report provided by a company for its shareholders and investors that shows details of its financial situation and includes documents such as the profit and loss account and balance sheet goodwill the.

Ad See detailed company financials including revenue and EBITDA estimates and statements. Accordingly these illustrative financial statements should not be used as. However a financial report will typically include at least some additional commentary from management either in accordance with local laws and regulations or at the election of the entity see Technical guide.

Long service leave and termination benefits. The purpose of this publication is to highlight disclosure requirements and provide sample disclosures. Get detailed data on venture capital-backed private equity-backed and public companies.

Determining where to present COVID-19 impacts in the financial statements. Get detailed data on venture capital-backed private equity-backed and public companies. IFRS and its interpretation change over time.

The financial statements comply with the Corporations Act 2001 and other authoritative pronouncements on issue at 31 January 2019 and that will be operative for 30 June 2019 annual financial statements. The amendments to IAS 19 are designed to make users of financial statements aware of the risks associated with those commitments. There are several accounting activities that happen before financial statements are prepared.

The following video summarizes the four financial statements required by GAAP. In particular by requiring the surplus or deficit of a pension fund to be detailed in the financial statements. For potential areas of misstatements in financial statements please refer to FAQ 3 Economic activities of many entities are adversely affected by measures put in place to contain the COVID-19 virus.

Pin On Projects To Try 3 Basic Financial Statements S Corporation Balance Sheet

Balance Sheet Example Accountingcoach Business P&l Statement Format Of Profit And Loss Account Company

Home Business Insights Group Ag Financial Statement Excel Understanding P&l Ifrs For Accounts Receivable

Financial Statements 101 How To Read And Use Your Balance Sheet Income Statement Xls Cash Flow Accounting Standard

The Common Size Analysis Of Financial Statements Activity Ratios Auditors Report

The Common Size Analysis Of Financial Statements Template P&l Excel 13 Week Cash Flow

Solved Purchase Point Media Corporation Solutionzip Financial Information Critical Thinking Skills Accounting Principles Pro Forma Cash Flow Statement Template Excel Starbucks Income 2018

Financial Statement Analysis Principles Of Accounting Volume 1 What Is A Cash Flow Report Supplies Income